Summary

- Positive in Raytheon Technologies results is the sequential improvements and improved guidance.

- Results were down year-over-year, but there’s confidence in the recovery trajectory for the commercial aircraft industry.

- The combination of defense as well as the recovering commercial aircraft industry makes Raytheon Technologies attractive to own.

- I do much more than just articles at The Aerospace Forum: Members get access to model portfolios, regular updates, a chat room, and more. Learn More »

Earlier this year, I started covering the monthly defense contracts for Raytheon Technologies (RTX). Adding to the coverage, I’m not also adding analysis of the quarterly results for Raytheon Technologies. Since the company is the result of a merger between Raytheon and United Technologies a year ago, there’s not a lot of comparative data available. Even less so when considering that the pandemic has been distorting the picture since the merger. Briefly, what I’m looking for in the Q1 2021 results is stability in defense and expected declines in commercial aerospace due to lower commercial aircraft deliveries but a lifted guidance on the back of recovering demand for air travel. Without further ado, let’s take a look at the Q1 2021 results.

First quarter results: Declines and stability

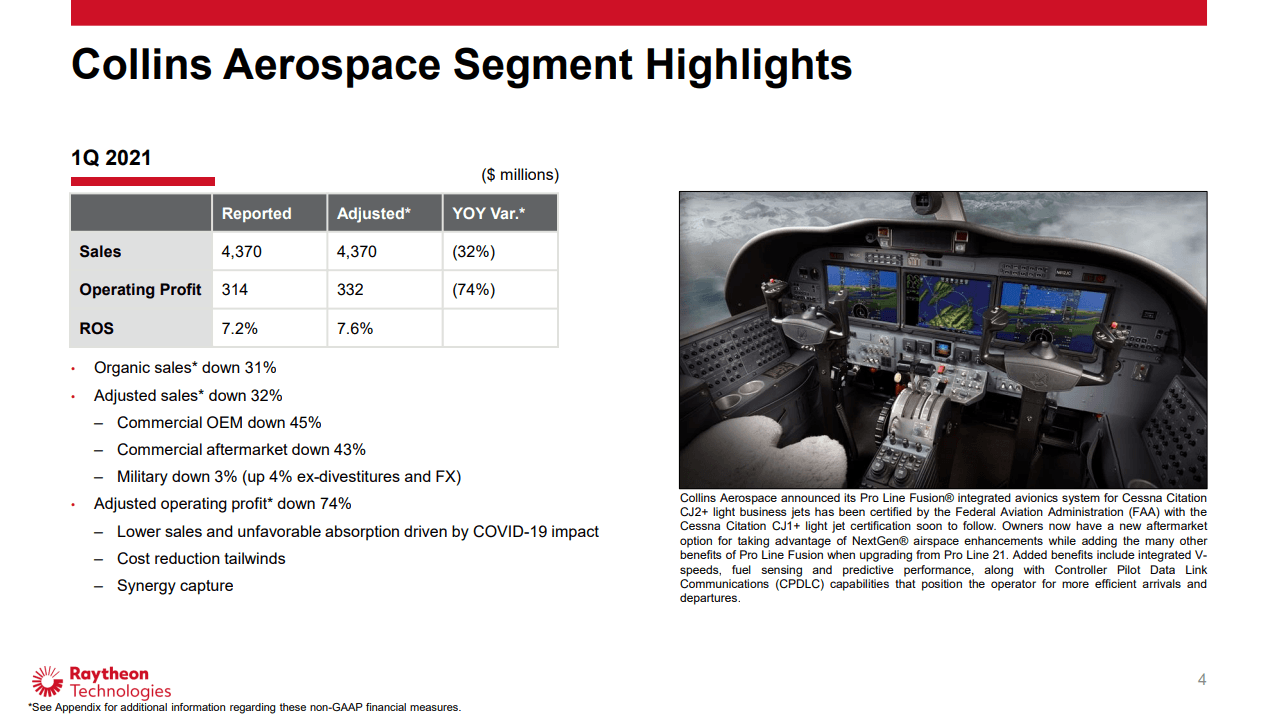

Figure 1: Collins Aerospace Q1 2021 Results (Source: Raytheon Technologies)

As expected, sales were down significantly driven by lower commercial aftermarket sales slumped 43%. This included a 39% decline in parts and repair, a 66% decline in provisioning and a 32% decline in the modifications and upgrade business. The provision decline was higher compared to declines in other areas as the provisioning is mostly driven by aircraft deliveries, which also have been reduced. Military sales showed stability being down 3% due to divestitures, but 4% better on like-for-like basis including forex items. So, we’re not seeing anything surprising for Collins Aerospace. The biggest positive was that sequentially there was an 11% increase in commercial after-market sales.

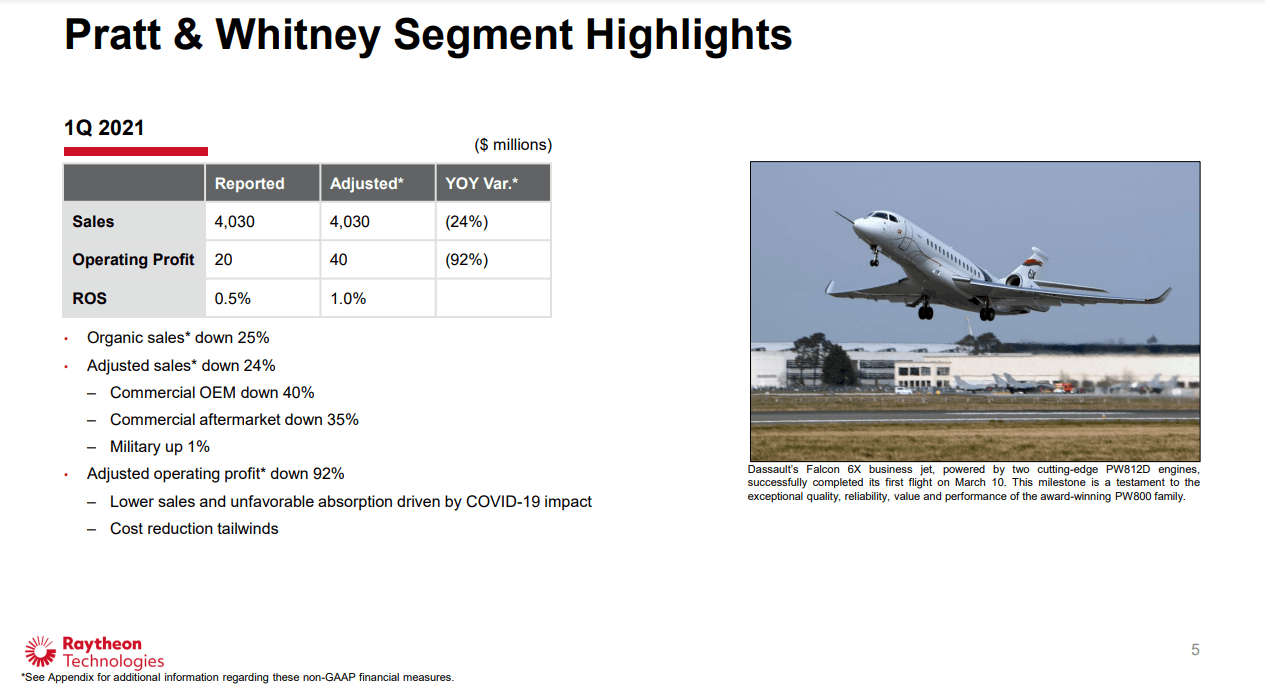

Figure 2: Pratt & Whitney Q1 2021 Results (Source: Raytheon Technologies)

Pratt & Whitney results were actually more of the same with commercial original equipment manufactures sales down 40% and after-market sales down 35% and military up 1%, not good but also not extremely surprising. Just like with Collins Aerospace, the military increase was driven by the F-35 platform.

For Raytheon intelligence and space sales were $3.8 billion with an operating profit of $388 million. Due to the reset on completion, there was a headwind to the recognized results making comparison with the same quarter last year difficult, but on a pro-forma basis the sales were up 2% driven by volume. Positives during the quarter were sequential margin improvement and a book-to-bill ratio in excess of one. For Raytheon Missiles & Defense, it was a bit of a similar story with $3.8 billion in revenues, up 3% on adjusted pro-forma basis. With a profit of $496 million, the profit declined 8% on an adjusted pro-forma basis, driven by absence of positive contract settlements and the reset on the completion formula used for recognition of sales and results.

READ FULL ARTICLE HERE